Earlier this month, a member of the US military was charged with insider trading after allegedly leveraging classified information to place a series of bets on Polymarket related to the US abduction of Venezuelan President Nicolas Maduro. This is just the latest scandal involving prediction market platforms – trading applications where users can exchange contracts on the outcome of real-world events.

Amidst a surge of media reporting and investigations into potential insider trades on these platforms – about everything from the Nobel Peace Prize, to presidential pardons, to US and Israeli attacks against Iran and even the weather – ACDC set out to determine whether these incidents reflect isolated, albeit recurrent, cases or a broader, systemic risk.

We analyzed all settled markets on Polymarket, one of the two main prediction market platforms along with Kalshi, and found that political markets with outcomes determined by groups of insiders display disproportionately high signs of trading on insider information. Within political markets, those related to military or defence actions show the clearest signs of widespread information asymmetries.

ACDC found:

🔴 Political markets drive a disproportionate share (over 36%) of the total trading volume across Polymarket despite being a small portion of total markets on the platform (4%).

🔴 Political market categories with the highest risk of insider trading (those determined by the decisions of an individual or small group of individuals in a military, executive branch or central bank) represent $8 billion in trading volume.

🔴 In most markets, the success of longshot bets (defined as a bet of $2,500 or more at a price of 0.35 or less, implying ≤ 35% probability) aligned with expectation: overall, 14% of longshot trades bought the winning outcome.

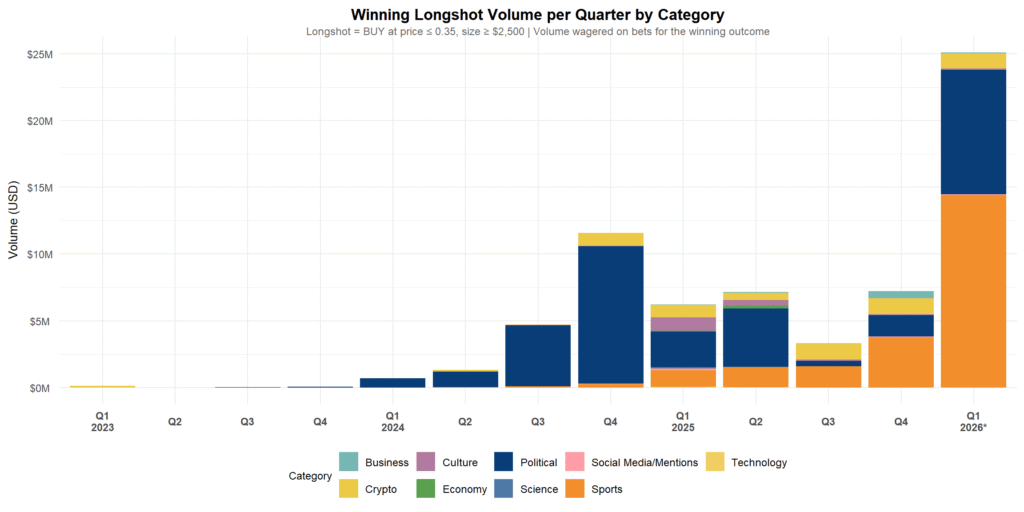

🔴 Political markets were the second most successful longshot bet category, with 25% of longshot bets succeeding, and the largest absolute volume of longshot bets placed on the winning outcome: we observed $35 million wagered in longshot bets, of which $9 million was bet in the first ten weeks of 2026 alone.

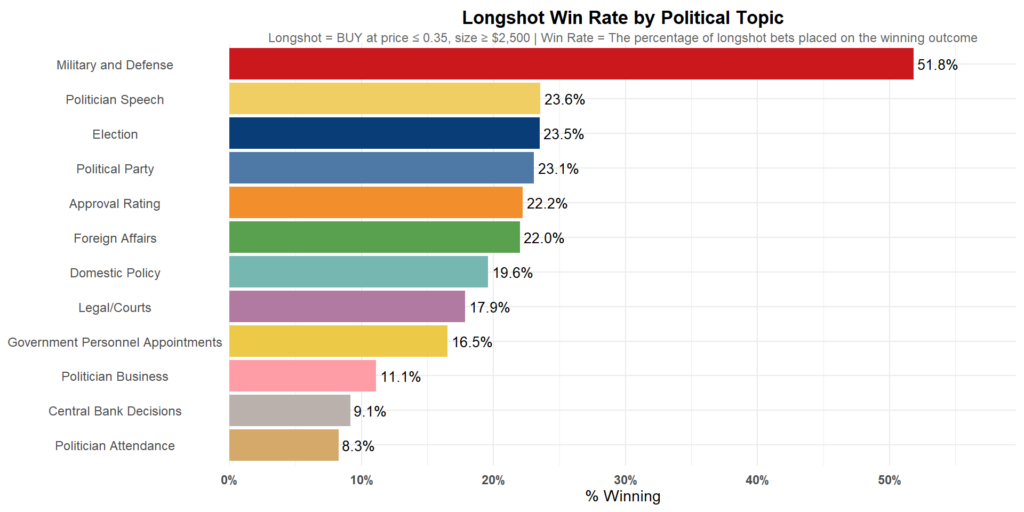

🔴 Within political markets, those related to military and defence events are a clear outlier, with a disproportionately high longshot success rate of 52%. There is a noticeable spike in successful longshot betting just before these markets resolve, with more longshot bets placed on the winning outcome than losing outcome in the twelve hours before the market closed.

What is Polymarket?

Polymarket is a prediction market platform where users trade on outcomes of real-world events using blockchain-based contracts. Users buy and sell contracts for an outcome (often Yes or No) priced between $0 and $1, with owners of winning contracts receiving $1 when the market is settled. Theoretically, prices reflect the implied probability of an event occurring, and the platforms have become popular with traders who profit by buying undervalued outcomes or selling overvalued ones before resolution.

Indicators of Insider Trading

Our analysis divides markets according to topic as well as who determines their outcome. We focus on political markets, which make up just 4% of settled markets on Polymarket, while accounting for over a third of total trading volume — $19.7 billion of $54.4 billion wagered since 2021.

We use three primary indicators of insider trading.

1. Successful longshot bets.

We define longshot bets as bets of $2,500 or more placed at prices of 35¢ or less, implying a probability of 35% or lower. In efficient markets these should win no more than 35% of the time. Across Polymarket as a whole only 14% win, yet political markets show a 25% win rate, with $35 million wagered on winning longshots. Across all markets, $25 million was wagered in winning longshot bets in the first ten weeks of 2026 alone.

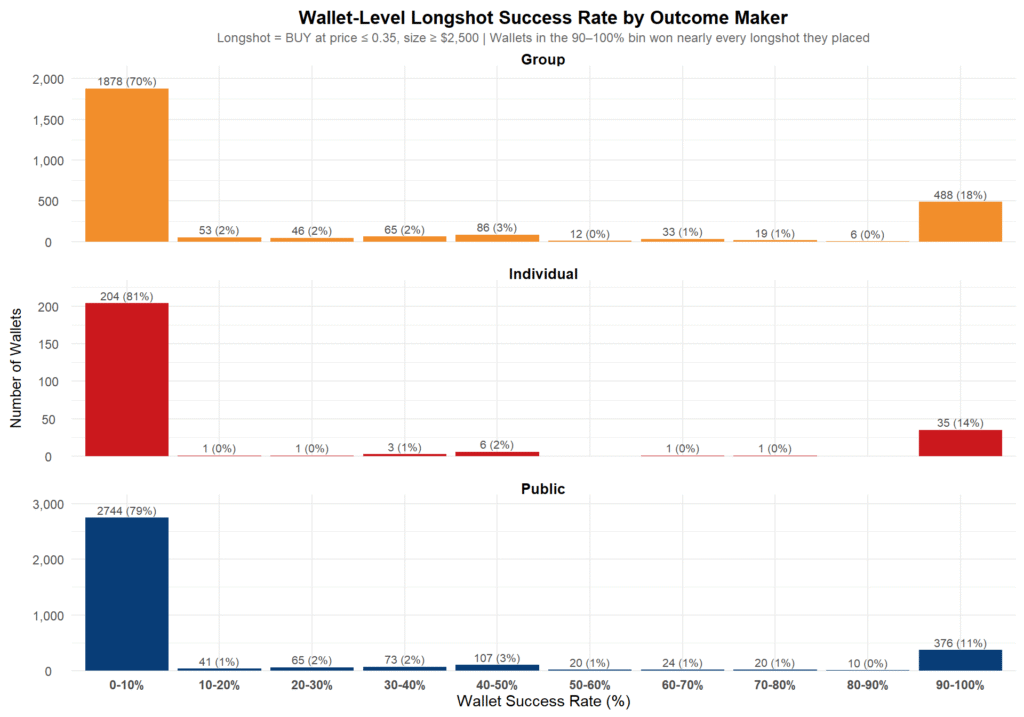

2. Wallet success rate

A small concentration of wallets that win on longshot bets at near-perfect rates. In low-risk public-outcome markets such as elections only 11% of wallets have a 90–100% success rate. In markets determined by groups or institutions, that share climbs to 18%, a pattern that is hard to explain by luck, skill, or general mispricing.

3. Timing of bets

Successful bets placed close to market resolution. In group-outcome markets, winning longshots cluster in the final hours before resolution, even when markets close early because the event has happened.

Military Markets Stand Out

Looking at defence and military markets in particular, we found a staggering 52% of longshot bets landed on the correct outcome. This is well above the 35% ceiling that prices would imply. These were driven by highly successful wallets placing well-timed bets. If we divide the last twelve hours before military and defence markets closed into two-hour windows, there are more winning longshots than losing ones in five out of the six two-hour windows. In total, $9.3 million was wagered on winning longshot bets in military markets.

The June 2025 US strike on Iranian nuclear facilities offers a striking case study. Across day-specific markets that resolved “Yes” after the strike, 19 longshot bets totalling $164,292 were placed in the hours immediately before the operation. Eight wallets walked away with $1.8 million in combined profit — one earning nearly $500,000 — despite the strike relying on deception, decoy bombers, and stealth aircraft that left no public signal of timing.

Group-outcome Markets Present the Highest Risk

Theoretically, political markets with outcomes determined by groups and institutions present the greatest risk of insider trading. These include military activities, central bank decisions, and actions from the inner circle of the executive branch. Even when a single official holds final authority, institutional decisions typically involve deliberation, planning and execution across a wider group. This expands the set of people with non-public knowledge.

Political outcomes determined by individuals, such as a president’s choice of clothes or the words they use in remarks to reporters, are easier to manipulate by the outcome maker, but the number of people with advanced knowledge is lower.

Finally, outcomes determined by the public, such as election results or approval ratings, carry the lowest risk for insider trading.

This is borne out by our analysis. Across all three indicators, group-outcome-maker markets outperform on indicators of insider trading: higher longshot success rates, more perfect-win wallets, and pronounced last-hour clustering of winning bets.

Interestingly, however, when we look at the distribution of win-only wallets for individual-decision markets, a small group of perfect-rate wallets is masked by a much larger pool of losing bets. This suggests that insider activity may exist even where category-level averages look unremarkable.

Political Markets are Not Unique

Because we are primarily interested in the corruption risks, our analysis focuses on political markets, where public officials and members of the armed services hold the inside information.

However, culture and sports markets also show signs of insider trading. Culture markets show the highest longshot bet success rates overall. Sports markets have nearly doubled their longshot win rate (from 5.2% to 9.4%) recently, driven by an explosion in highly precise markets about individual players, where information asymmetries are easier to exploit.

No More Wack-a-Mole

The open and pseudonymous nature of activity on Polymarket means that regulation or legislation that relies on policing individual users will be difficult to enforce. Systemic risk calls for systemic solutions.

ACDC supports a regulatory approach that prohibits or restricts categories of political markets most vulnerable to insider trading, particularly those with group outcome makers, rather than only prohibiting categories of individual users from betting on certain markets.

The Commodity Futures Trading Commission (CFTC) has the authority to ban contracts on events that it decides are not in the public interest, including those related to assassinations and war. It should also declare a broader selection of political markets on outcomes determined by individuals and groups of insiders as contrary to the public interest. The inherent risk of information asymmetries mean these markets are not a fair and level playing field.

We also recommend that Polymarket should be required to collect government-issued identification for all bettors. Bets identified as suspicious could also be held and not paid out until the bettor’s identity is verified and any potential conflicts of interest are assessed.

This research was supported by a grant from the John D. and Catherine T. MacArthur Foundation.

Insider Risks in Polymarket Political Markets

Insider Risks in Polymarket Political Markets

Related Articles

Reports

Reports

The Leniency Lobby: How the U.S. Lets Global Corruption off the Hook

Alleged criminals and corrupt politicians from around the world are spending millions to lobby for political support, pardons and sanctions relief in Washington, according to analysis of Foreign Agent Registration Act (FARA) filings by ACDC.

Reports

Reports

Find the Needles, Analyse the Haystack

This report shares findings and insights from the first phase of the Illicit Finance Data Lab, an initiative by ACDC and OCCRP to help scale up meaningful collaboration between investigative journalists and academic researchers working on illicit finance.

Reports

Reports

Inside the Congo Hold-Up

How a high-level financial operation transformed a privately-owned bank in the Democratic Republic of Congo into an engine of grand corruption.